Coatings R&D 2004: Meeting Cost and Regulation Expectations

Recent signs that the economy is picking up steam is reflected in anticipated increases in research and development budgets and staffs of coatings manufacturers. But the pressure to cut costs, meet environmental regulations and maintain quality and competitiveness is as great as ever.

That's part of the research and development picture for 2004, according to the results of a survey sent by Industrial Paint & Powder to R&D managers of paint and powder coating producers that supply industrial original equipment manufacturers (OEMs) and custom coaters. The survey responses disclose current research efforts, detail research budgets and reveal where R&D is headed in the near future.

Nearly 25% of respondents say they will increase their spending budgets. That compares with less than 20% of last year's respondents and about 17% of respondents two years ago who were planning to increase R&D spending. However, the percent planning increases is still significantly less than it had been for several years preceding 2002.

The number of respondents indicating that they will decrease R&D spending fell slightly from last year to about 6%. A little more than two-thirds of respondents say their budgets will remain the same this year.

Of those respondents planning to increase their budgets, one-third say the increase will be from 10 to 19%. Nearly another third say they will increase their budgets by less than 5%. The rest will see budget increases of 5 to 9% (22% of respondents), 20 to 29% (11% of respondents) and 30 to 49% (3% of respondents).

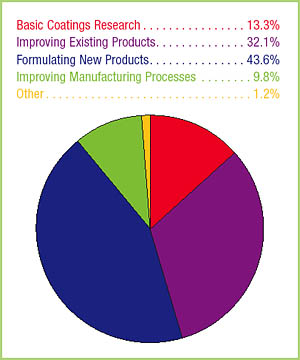

The percent of R&D budgets that companies will spend on general research categories closely resembles last year's spending. Efforts to formulate new products will receive nearly 44% of respondents' 2004 budgets. About 32% of the funds will be spent on improving existing products. The rest of the budget will be nearly split between basic coatings research and improving manufacturing processes.

Where's the money going?

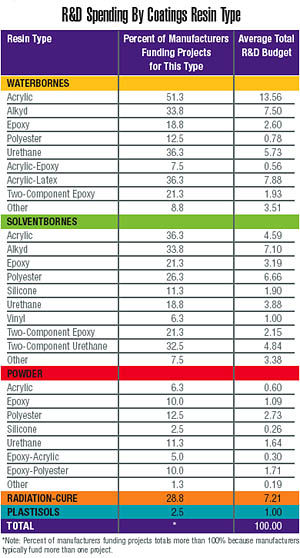

In recent years, manufacturers have budgeted the bulk of their R&D funds-about 44% for 2004-for waterborne coatings. Respondents indicated that they would spend roughly the same percent of the budget as last year on the various types of waterborne coatings. Research on acrylic and acrylic-latex will account for a little less than half of the money spent on waterborne R&D. A little more than half was spent on the two types last year.Solventborne coatings are still widely used and will receive nearly the same percentage of respondents' R&D dollars as last year. Nearly three-fourths of all respondents are devoting some of their budgets to solventborne products, accounting for nearly 39% of R&D spending.

Research on two-component epoxy and acrylic solventbornes, which accounted for nearly 40% of the budget for solventborne coatings two years ago, will account for 21% this year. Of all spending on solventborne research, alkyds will receive the most, followed by polyester.

Nearly 80% of all coatings manufacturers are performing some research on waterborne coatings. More than half of the respondents say they are working on acrylic waterborne coatings. About 36% of respondents are funding R&D efforts on urethane waterbornes, up substantially from last year. About the same percent of companies are also working on acrylic-latex waterbornes.

In powder coatings, more than 12% of respondents say they are planning R&D efforts on polyester powder coatings. The next two categories of powder coatings garnering the most attention are urethanes and epoxy-polyesters, respectively. Figure 4 shows this year's plans for R&D development in all resin categories.

Reasoning behind R&D efforts

When companies assign portions of their budgets to various coating technology categories, they assign primary objectives to each category (Figure 6). For waterborne coatings, the most important objective is lowering costs, according to nearly 77% of respondents funding R&D efforts in this area. Improving performance is important, though less so to respondents than in the past. A little over half of respondents listed it as a primary R&D objective, compared to 64% a couple of years ago.Though lowering solvent usage and HAP and VOC content is less important a priority than it had been in the past, it's still a major priority. For waterborne, high-solids and two-component coatings, lowering VOC and HAP content is the second-most-important priority after lowering costs.

Lowering costs has become increasingly more important to formulators. It ranks as a high first priority in each category of coating, and the percentage of respondents saying lowering costs is a primary objective has increased in the high-solids and radiation-cure categories.

In the powder coating category, nearly 67% of respondents cited lower cure temperatures as a primary R&D objective, up from 53% last year. Expanding color selection was also cited as primary objective significantly more this year than last, while improving chargeability for electrostatic application, reducing film defects and improving reclaimability were cited far less this year than last as primary objectives.

Pinching pennies

In the comments section of the survey, more than one in four respondents listed costs, in one way or another, as their greatest challenge. About 15% of respondents listed environmental issues or government regulations as their biggest challenge.

Last year, environmental issues and regulations shared top billing as the most important challenge facing respondents with a sense that they were being squeezed-having too many responsibilities, projects, etc. These two issues were cited by more than 44% of respondents last year as their greatest concern. This year, only about 8% listed a lack of time or resources as their greatest challenge.

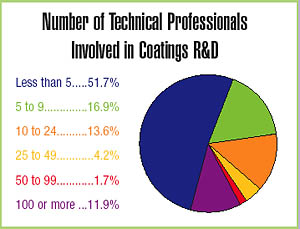

SIDEBAR: RESPONDENT PROFILE

Research and development managers from 160 U.S. manufacturers of paint and coatings responded to Industrial Paint & Powder's annual R&D survey. OEM coatings represent an average of more than 55% of the business for the typical respondent's company. Nearly 28% say the OEM market accounts for 90 to 100% of their business, while more than 58% say the OEM market accounts for 50% or more of their business.

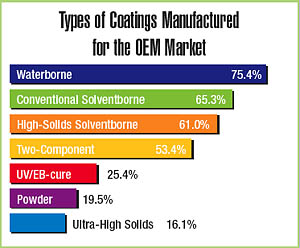

For the last seven years, more companies (75%) have manufactured waterborne coatings than any other type. Waterborne coatings are followed by conventional solventborne, high-solids, two-component, UV/EB-cure coatings, powder and ultra-high solids (Figure 1).

Annual sales in volume to the OEM market rose steadily and significantly (the value of those shipments has risen more slowly) in recent years, from 398 million gallons (data for powder coatings are collected in pounds and converted to gallons) in 1996 to 453 million gallons in 2000, according to U.S. Census Bureau figures. Shipments fell to 407 million gallons in 2001 and rose to 412 million gallons in 2002. Shipments for the first half of 2003 were 210 million gallons.

About 70% of respondents in the survey report their sales as less than $10 million; 18%, less than $1 million; $10 million to $24.9 million, 11.4%; $25 million to $49.9 million, 3.5%; $50 million to $99.9 million, 6.1%; $100 million to $249.9 million, 4.4%; and $500 million or more, 4.4%.

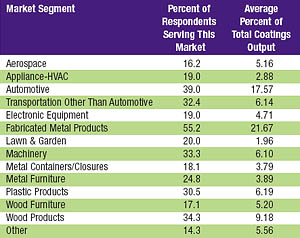

The top OEM market served by respondents is fabricated metal products, with 55% of respondents serving it (Figure 2).

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!