TiO2 Optimization

Efforts and Current Market Trends

The last several years have been a roller coaster ride for anyone associated with the TiO2 industry, including raw material suppliers and both producers and consumers of TiO2 pigment products. The unprecedented volatility in the supply and demand balance, and subsequent rapid increase and collapse of TiO2 pricing led many consumers to take measurable action to restrict use of the product more than at any point in the past 20 years.

TZMI believes that significant R&D efforts were put forward by formulators from 2010 through 2013, but efforts to reduce TiO2 usage in formulations have waned as the price for the compound that is critical to providing opaque properties to mixtures has substantially declined during the past 18 months. The risk of supply shock has also declined as inventory levels throughout the supply chain remain healthy. TZMI believes that many formulators have instead shifted focus to optimizing formulated costs, which has different implications versus a ‘decrease use of TiO2’ strategy. The latter approach often includes efforts to minimize TiO2 wherever possible, and this tactic was widely employed during 2010-11.

TZMI’s research concludes the following regarding TiO2 optimization efforts.

- Formulators are less focused on TiO2 now than in the past three years.

- Optimization efforts are once again focused on formulation cost optimization rather than TiO2 minimization, although the two often go hand-in-hand.

- TiO2 reduction efforts have lowered TiO2 global demand by 3-5% permanently, equivalent to more than US$400 million per year in lower sales.

- The evolution of the Chinese TiO2 supply base and coordination efforts with multinational formulators offers the greatest short-term potential for optimizing TiO2-related cost (and potentially overall formulation cost).

TiO2 Optimization

The use of TiO2 pigment in many coatings formulations is essential. Rutile TiO2 has one of the highest refractive indices (RI) of any economically viable pigment used in formulations, with a value of 2.73. By comparison, air has a RI of 1.0, and most particles used in coatings formulations have RI values of 1.4-1.7. Therefore, TiO2 raises the average RI of the formulation, generally leading to a higher overall opacity. Substitutes and extenders for TiO2 pigments include aluminum silicate minerals, clays, calcium carbonate and hollow-sphere pigments.

Specifically, the light-scattering efficiency of TiO2 is a function of several factors including the refractive index of the coating formulation relative to the RI of TiO2, the distribution and mean particle size of other pigments and extenders, and the pigment volume concentration (PVC) of the formulation. Part of TiO2’s ability to provide hiding power is attributed to optimal spacing of the particles. The use of extenders in coating formulations can improve spacing of TiO2 particles – particularly as the particle size distribution of the extender gets closer to that of TiO2, but the use of larger extender particles and/or significant extender volume concentrations relative to TiO2 reaches a point at which the hiding power of the formulation can either decrease materially or not improve further.

Hollow-sphere pigments (HSPs) are more of a classic substitute for TiO2. These products are typically styrene/acrylic polymers and have been around for more than three decades. HSPs are added to the formulation and contain water molecules surrounded by a spherical ‘bead’ polymer structure. As the coating dries, the water diffuses outside the ‘bead’ structure, leaving an air void. HSPs lower the overall RI of the formulation and, as such, increase the light-scattering efficiency of the TiO2 used in the formulation. HSPs are used most frequently in high TiO2-containing formulations with a PVC that is usually below the critical pigment volume concentration (CPVC), which is the maximum filled pigment/binder matrix. Formulations that use high levels of HSPs tend to have low wet hiding power (appear less opaque when applied). HSPs can negatively impact critical formulating properties such as scrub resistance and coating durability.

Practical Use of Substitutes

TZMI believes that the use of substitutes such as HSPs occurred more in the past several years than in the prior decade as the supply shock that occurred in the TiO2 market drove formulators to consider all potential options to maintain production levels necessary to serve customers.

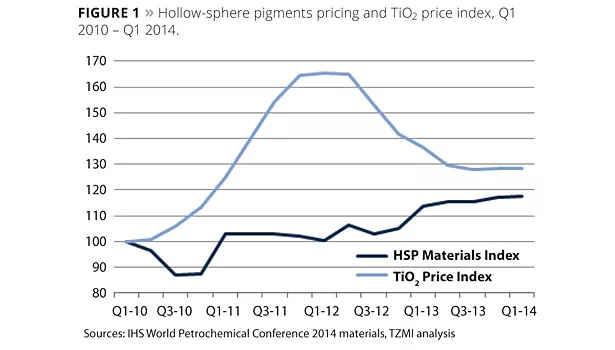

Figure 1 provides an estimate of pricing evolution for HSP raw materials and TiO2 since 2010. TZMI believes that this figure illustrates the incentive for using more HSPs that occurred in the price spike of 2011/12. The incentive to use HSPs now is significantly lower than in 2011/12.

Inorganic extenders and pigments such as kaolin, calcium carbonate and other aluminum silicate clays were used to a greater degree in the past several years as the under-supply situation led formulators to take actions that were not optimal but were necessary. In some cases and in some formulations, the use of some inorganic substitute products has been lowered to historical ‘normal’ levels following the supply shock of 2011/12. TZMI also believes that these products are often priced at a discount to TiO2 (and have been for many years) and nearly always have arbitrage value over TiO2. In many cases, the use of these materials has been optimized for years.

For some inorganic substitutes, however, innovative producers have been able to lower the mean particle size and improve the particle size distribution. This improvement in technology has improved the efficacy of these substitutes for use as extenders and enabled formulators to incorporate the products more permanently into formulations where properties allow for greater use. The gains experienced by formulators vary based on numerous factors (resin chemistry used, PVC level in formulation, properties desired in the coating, etc.), and not everyone agrees that these products have made a significant impact on TiO2 use. Like other extenders, the use of these substitutes has a practical limit, and TZMI believes the greatest gains in this area have already occurred.

Formulators continue with programs to use innovative products, although TZMI believes these programs have decreased in priority level as the supply shock of 2010/11 is now in the rear-view mirror and TiO2 prices have declined significantly. Additionally, the arbitrage between TiO2 pricing and the base raw materials used to produce many of the organic products follows a trend similar to that noted in Figure 1.

Notably, in Valspar’s Q2 2014 earnings call, CEO Gary Hendrickson stated, “The answer is, I don’t think about TiO2 much anymore. We have done a nice job of substituting somewhere in the high single digits over the last three years or so.” In PPG’s Q4 2013 earnings call, CEO Charles Bunch said in reference to TiO2 reduction efforts, “I think that we’ve capitalized on the best or quickest opportunities that we had…we are still working, but I don’t think we’re going to see the kinds of reductions that we saw in 2012 and 2013.”

From TZMI’s informal surveys of the market, the company estimates that long-term TiO2 global demand (all applications, including coatings) has decreased by 3-5% compared to pre-2011 levels as a result of optimization efforts, with some formulations optimizing TiO2 use by more than 10%. TZMI’s demand modeling now reflects this level of demand destruction globally, which TZMI estimates equates to reduced annual sales exceeding US$400 million for all TiO2 producers.

China TiO2 Products

Unlike the trend in substitution, TZMI does not expect the trend of using more China TiO2 products to abate. In fact, TZMI expects China TiO2 products, which are currently priced at significant discount (usually in excess of 15% of global average price) to western TiO2 products, to be used more frequently in the future. Figure 2 illustrates the increasing use of China TiO2 products in the Americas.

In North America, where the supply chain is more complicated and formulations are generally more demanding, the use of China TiO2 products has been historically limited to less than 10% except during the supply shock of 2011/12, where China TiO2 usage increased to nearly 14% of demand in the region. Usage levels have declined to approximately 6% currently, which is still above pre-2011 levels that averaged only 3%.

In Latin America, the use of China TiO2 products has steadily increased and currently stands at approximately 25% of the demand in the region. Likewise, the average price difference in TiO2 between Latin America and North America has increased over time. While not as dramatic, the use of the China TiO2 products in many parts of Asia has also increased. These products are almost entirely used at the expense of higher-quality western TiO2 products.

The relative greater use of China TiO2 products in Latin America reflects the differences in supply chain dynamics, the lack of domestic supply, and the cost versus quality focus of Latin American formulators versus counterparts in North America. The last of these regional nuances is not limited to Latin America; it is a phenomenon noted in many emerging Asian countries where China TiO2 products are ‘fit for use’ in the applications where they are formulated. Western TiO2 products continue to be used in durable applications (most protective coatings applications) where the Chinese producers have generally been less successful in developing quality suitable for universal adoption.

TZMI believes that many, if not all, of the top coatings formulators have dedicated China TiO2 supply strategies. Many of these strategies have been made public, including agreements between Henan Billions and PPG, and Akzo Nobel and Guangxi CAVA.

TZMI believes that the Chinese TiO2 producers will need to continue to climb the quality curve and that this evolution will continue through co-operation with formulators and increases in know-how gained by Chinese TiO2 producers.

As stated by Sherwin Williams’ CEO Christopher Connor during its Q4 2013 earnings call, “I think we’ve commented that, at some point in time, perhaps 5% of our needs could be moved to that type [Chinese supply], and we’re seeing some progress towards that.” Comments from Valspar in the Q2 2014 affirmed that its firm was sourcing a significant volume from China as well. TZMI expects this trend to continue.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!