Paints & Coatings 2022: Understanding the Chemical Industry and Current Challenges for Coatings and Adhesives, Part Two

As discussed in Part 1 of this article, published in March 2022, chemical businesses have spent the last two years "fighting fires" as COVID-19 put the industry's resilience to the test — dealing with supply-chain disruptions, greater feedstock volatility, shifting customer behavior and rising costs of doing business. As of the writing of Part 2, another black swan event has added to global concerns — the invasion by Russia into Ukraine.

2022 Outlook

Until now, in 2022, analysts anticipated a more "moderate" environment that would be beneficial to vast areas of the broader chemical market, with slight concerns regarding potential setbacks from the Omicron variant or weather impacts. As of this writing, both of those concerns seem “under control”. However new concerns may have a greater impact than anything experienced thus far in the decade.

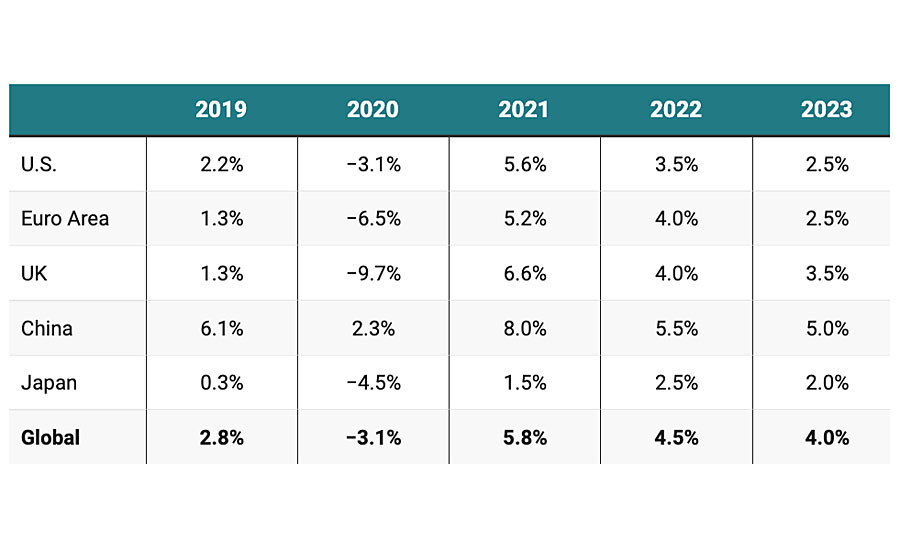

While inflation will certainly remain a story in 2022 (and likely into 2023), many expected it to be less "shock driven" and thus more stable/controlled. Economists are still calling for relatively robust growth, with global GDP expected to come in at 4.5% in 2022 and a still solid 4.0% in 2023 — down from 5.8% in 2021 (Table 1), but uncertainty looms.

Looking at a host of the more important end markets for the chemical space, we expect to see:

- U.S. housing also pushing higher (new home builds are up 2.5%, existing homes are up 3.1% in 2022, albeit predicted slowing in 2023 on rising rates).

- Global auto OEM up 9.0% in 2022 (with strength in the second half of 2022 as the global semiconductor issues moderate) and pushing still higher in 2023.

- Global semiconductor volumes up 16.5% in 2022 with a solid outlook for 2023.

- Global aerospace builds up ~32% as they come off their 2021 lows.

While the above depicts a stable atmosphere, there is uncertainty in the air especially related to:

- Interest rates rising — Fed signals it will likely hike interest rate to curtail inflation. The hike would be the first in over three years, and it would start off a rush of three or more quarter-point hikes this year aimed at taming rapidly rising consumer prices.

At this moment, the end market demand environment remains strong with housing, autos, semiconductors and aerospace expected to grow strongly.

Housing

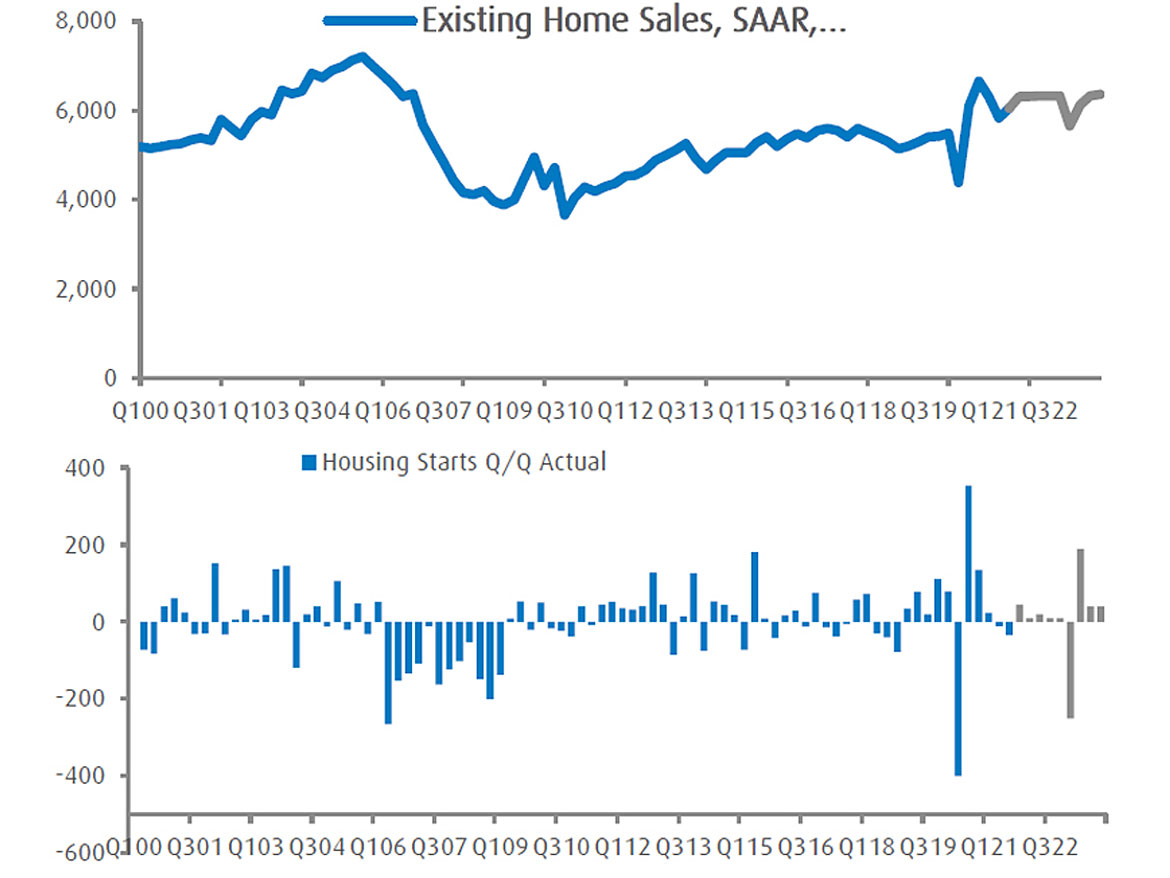

In 2021, new home construction increased by 12%, while existing home sales increased by 8%, as limited inventory and continued demand for housing drive solid strength — tempered modestly by rising rates and limited labor availability for new home construction. Looking ahead to 2022 and 2023, economists anticipate the picture improving in the short term, but fading as interest rates rise (Figure 1).

According to economists, existing home sales are predicted to climb 3.1% (to 6.32 million units) in 2022, while new home construction is expected to rise 2.5% (to 1.63 million units). While increased housing demand may support stronger growth, ongoing labor shortages are projected to limit new home construction, while rising prices and mortgage rates are expected to slow the pace of existing home sales.

Looking to 2023, economists see a more modest ~2% outlook for new home builds, while existing home sale growth is expected to drop to less than 1% as a series of expected rate increases in 2022/23 nick turnover in the market (Figure 2).

Housing — Impact on Coatings

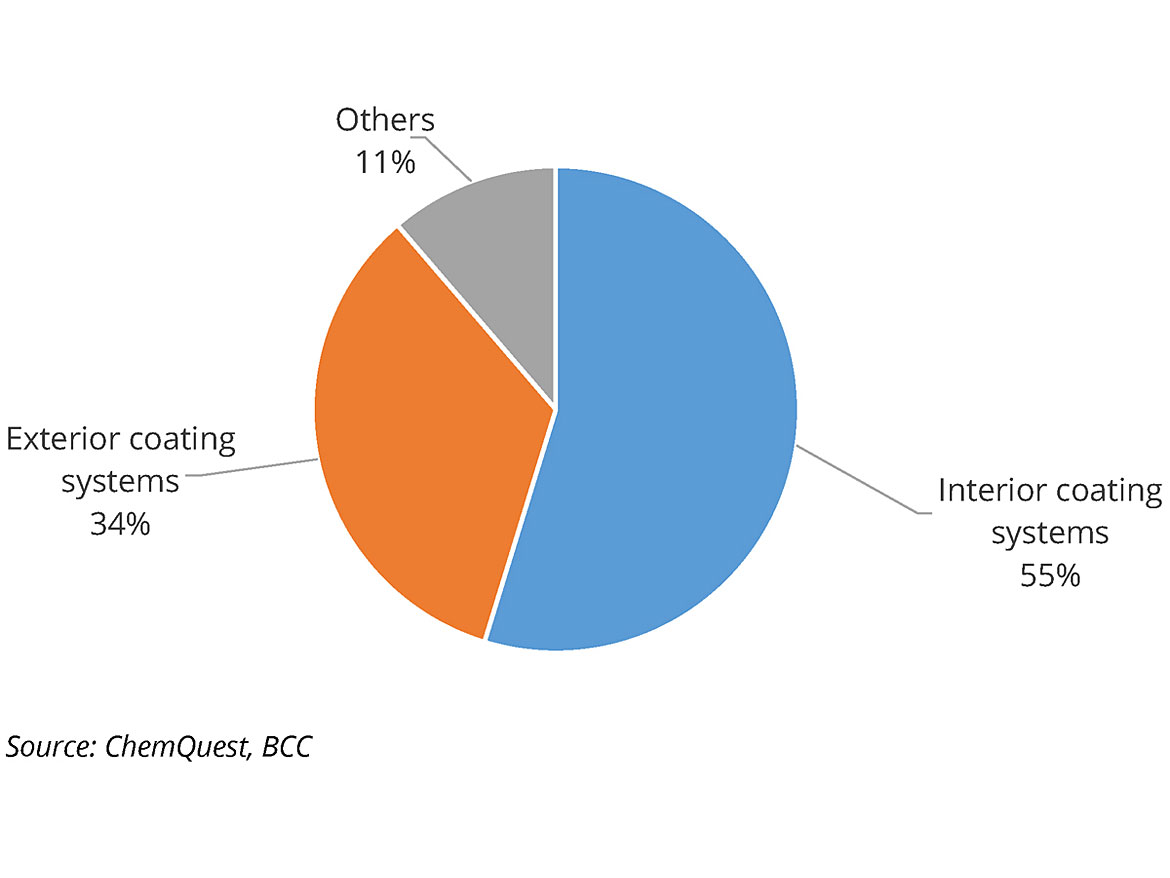

Coatings are heavily utilized in housing — better known in the industry as architectural paint. The architectural paint and coatings market is generally divided into interior and exterior paints and coatings (Figure 3).

Architectural and decorative paints and coatings are generally considered to be those paints and coatings intended for on-site application to residential, commercial or institutional buildings, by both amateur DIYers and professional painters. These include both external and internal paints and coatings.

A major portion of architectural paints and coatings is consumed by professional contractors, with the rest consumed by DIYers. A professional contractor will use more economical interior paints and coatings, and solventborne products for exterior applications. A DIYer will use more expensive interior paints to avoid the labor of repainting, as well as easier-to-use water-based paints. Almost 50% of architectural paints and coatings are sold through company stores, with the remaining sold through mass merchandisers and independent dealers such as paint dealers, hardware stores, lumberyards and decorating centers.

In general, these paints and coatings protect surfaces against a variety of external and environmental factors such as sunshine, UV radiation, acid rain and corrosion, and are applied to a variety of surfaces to improve appearance, corrosion resistance, adhesion and scratch resistance. Acrylic, epoxy resin and polyurethane coatings are some of the most often utilized construction coatings today.

Architectural coating demand is driven by multiple indicators: private/public investment, short-term interest rates, employment, homeownership, property maintenance and commercial building rates.

Housing — Impact on Adhesives and Sealants

One of the largest market areas for adhesives and sealants is in the building and construction industry. Industry growth is directly influenced by trends in construction spending, as adhesives and sealants find application throughout the entire industry.

There is a myriad of applications where these products are used. Major end uses for adhesives and sealants include the construction, repair and remodeling of residential and nonresidential structures; various nonbuilding projects (including highways and roads, bridges, tunnels and other civil engineering works); and utility infrastructure (such as dams and reservoirs, and water, electrical and gas distribution systems).

The sealants area of the industry, which accounts for a bigger part of demand in building applications than adhesives, is primarily focused on the construction market. All major adhesive and sealant product segments are represented in the construction market.

Improving construction sectors in the U.S. and Western Europe will further benefit the market. Strong advances in construction activity in the Asia/Pacific region are expected to fuel rapid gains in demand, driven by growing urban populations, rising household incomes and government infrastructure spending.

Automotive Market

After beginning 2021 with high hopes for a rebound in auto production levels, the year turned into a supply chain whack-a-mole game. The industry has been plagued with seemingly nonstop issues from semi-conductor chip shortages compounded by the Renasas production plant fire, the Texas Freeze, Malaysian lockdowns, and other factors. 2021 production ended flat (+1.2 %) year over year vs. expectations at the beginning of the year up 13.7%.

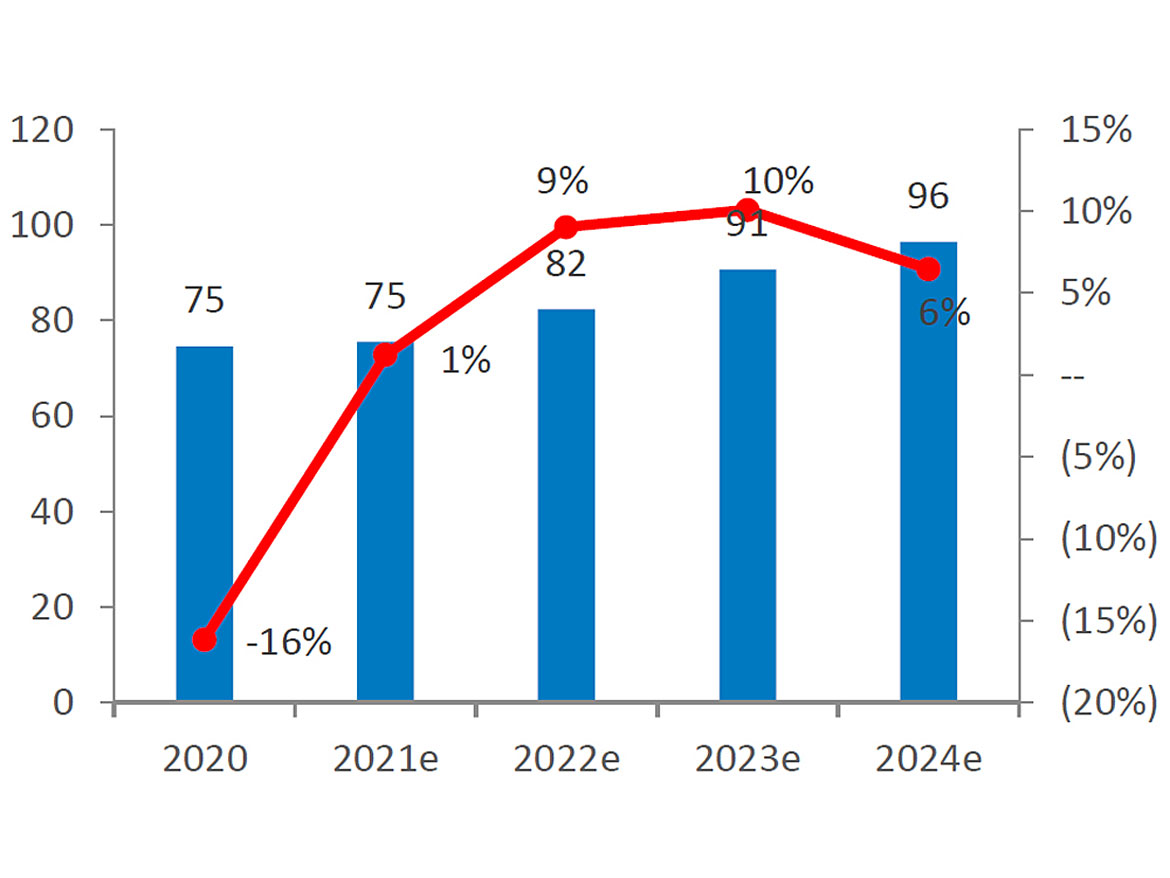

There are signs that supply chain kinks are being ironed out, predicating a multi-year rebound in vehicles, with 9% growth in 2022 and another 10% increase in 2023, before settling at 6.5% in 2024 (to 96.4 million units up from 89 million in 2019) (Figure 4).

North America, Europe and China are the three key markets, as they are expected to account for ~70% of global auto production (China ~30%, Europe ~22% and North America ~18%):

- North America: Production volumes are expected up ~17% year over year in 2022 following the disappointing ~0.6% decrease in 2021. Substantial increase to be driven mainly by the normalization of the supply chain primarily in the second half of 2022.

- Europe: Production is expected to be up ~18% year over year in 2022 following a ~5% decrease in 2021. A snapback is expected to be driven by the strong auto demand in Western and Eastern Europe assuming the economies reopen by mid-year 2022. Additionally, the region should benefit from strong export demand, which is expected up by double digits in 2022.

- China: Production should rise to a modest ~2% following its flat production in 2021 (and only 4% decline in 2020). China has managed the chip shortage far better than most geographies, as demonstrated by Chinese 2021 production levels only 4% below 2019 levels vs. 26% for Europe and 21% in the U.S.

The chemical industry has significant end-market exposure to the automotive industry, ranging from decorative applications (coatings, laminates) to safety and environmental applications, as well as base materials such as plastics, sealants and adhesives, which provide valuable light-weighted structural components that are becoming increasingly important as the auto industry shifts toward ESG-friendly solutions.

Auto — Impact on Coatings

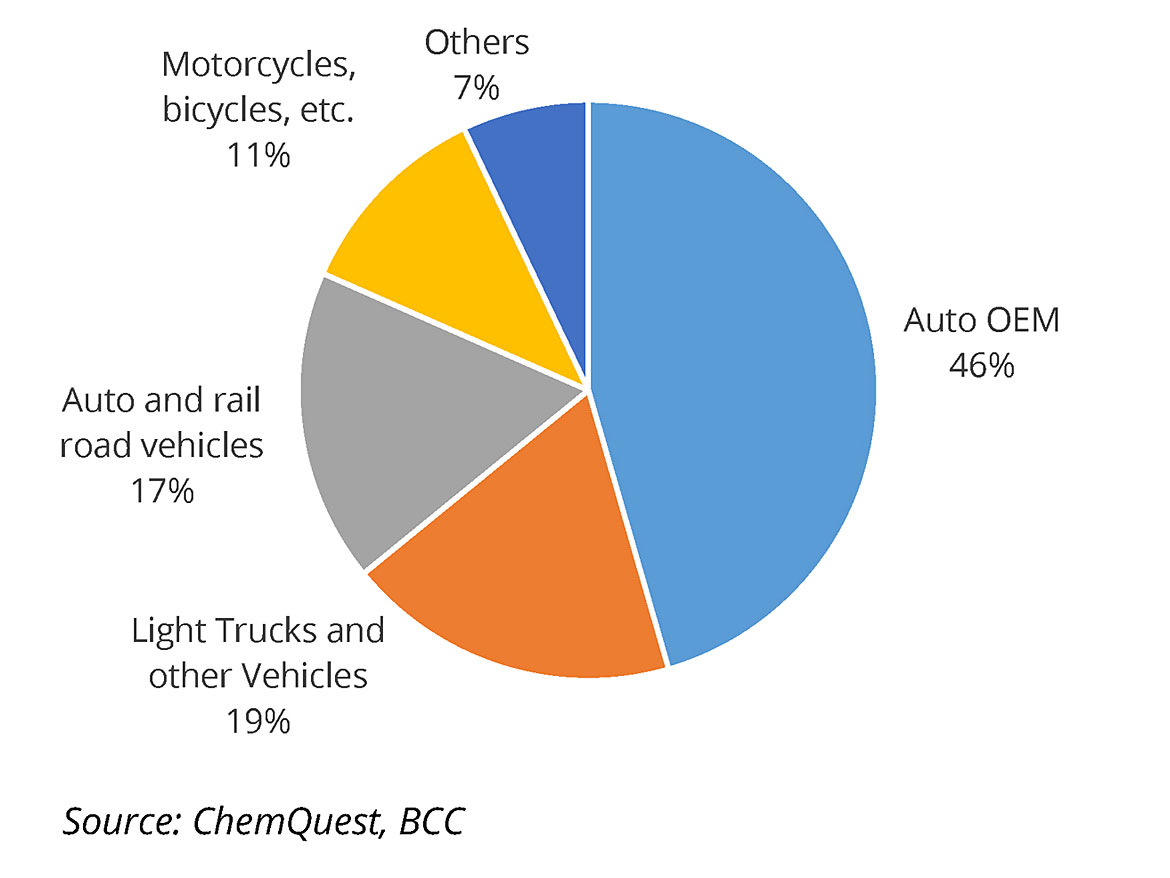

Vehicle paints and coatings include finishes for autos, vans, light trucks, sport utility vehicles, heavy-duty trucks, buses, trailers, campers, recreational vehicles and their component parts (Figure 5). The most important feature identified by the vehicle-buying public is a glossy and durable finish.

The painting of automobiles is arguably the most complex application in the field of industrial coatings. High levels of corrosion and weathering resistance are required, but the visual appearance is also critical. The following paints and coatings are common in automobiles: metal surface pretreatment, primer surfacer, primer, base coat and clear coat (for metallic finishes). Overall, the role of paints and coatings goes far beyond their application on exterior body panels and vehicle finish improvements.

Automotive paints and coatings have shown very significant growth, driven primarily by the increase in car ownership in developing markets. The automotive paint and coating market is, to an extent, based on the number of cars produced. Global car manufacturing continues to rise, with South America and other Asian-Pacific countries growing at a higher rate than Europe, North America and Japan, which are more established markets.

Auto — Impact on Adhesives and Sealants

The use of adhesives for automotive applications is widespread, from something as small as a sensor to something as large as a vehicle chassis. There are numerous applications for adhesives and sealants in motor vehicles, including interior, exterior and under-the-hood uses. Automotive OEMs are increasingly employing structural adhesives in place of, or in conjunction with, mechanical fasteners, as they work to reduce vehicle weight, and lower material and assembly costs.

High-performance adhesives play vital roles in the quality of both interior and exterior transportation components. Adhesive technologies provide strong bonding capability in joining similar and dissimilar materials. Adhesives are used in lighting, headliners, instrument panels, seats, trim parts, carpet attachment, door panels, glass bonding, and flange and hem sealants. Applications of adhesives in transportation offer extremely diverse bonding challenges. The transport sector uses high-strength adhesives in a wide range of applications, as bonding is a suitable method for the most common materials in this sector.

Raw Materials and Commodities Outlook

Looking into 2022, analysts expect a reasonable amount of variance within the raw material chain. Following a year in which "everything went up," 2022 was expected to be more nuanced. As of this writing, most major petrochemicals are uncertain whether they will fully recover from the outage-driven/supply-shock experienced in 2021.

Oil and Gas

Global oil demand has recovered to pre-COVID-19 levels of around 100 million barrels per day, with strong demand in the United States and Asia. Notably, U.S. gasoline demand achieved record highs this past summer while Asia demand resumed its two-decade-long growth streak. According to JP Morgan, global commodity markets have surged to multi-year highs, with oil prices topping $130 per barrel, while natural gas, aluminum and wheat have all hit fresh record highs since Russia’s invasion of Ukraine and the subsequent sanctions that have been imposed on Russia as a result. An extended period of geopolitical tension and elevated risk premiums across all underlying commodities is now expected, with far-reaching implications across global commodity markets. The unfolding conflict has vast implications, and J.P. Morgan Research has revised commodity price forecasts up 10-20% across the sector. Russia's impact on the global energy balance is meaningful.

In the case of natural gas, Russia is the second largest producer of natural gas globally, accounting for 16.6% of total global natural gas supply in 2020. Until now, about 70% of Russian exports were sent to Europe by pipeline, and the region has relied heavily on Russian gas transiting through Ukraine.

Overall, if the market begins to price a probability that Russia may take retaliatory measures by reducing its energy exports, a four-month disruption of 2.9 million barrels per day (mbd) of Russian export volumes to Europe and the U.S. will likely see the Brent oil price averaging $115/bbl in 2Q22, $105/bbl in 3Q22 and $95/bbl by 4Q22, according to JP Morgan.

Olefins and Polyolefins

Olefin and polyolefin pricing is estimated to fall in 2022 and 2023 after a record year in 2021. New capacity, increased inventory levels, the lack of major weather events (Texas Freeze, Ida and Nicholas), and freight bottlenecks that prevented global arbitrage opportunities from balancing parts of the market starting to alleviate in late 2022 and 2023 would all contribute to this. All of this will counteract what should be reasonably strong demand because of the macroeconomic rebound.

Global Logistical Issues Are Likely to Remain High for the Rest of 2022; Perhaps Even Longer

The persistence and worsening of global logistics difficulties, which were compounded by increasing shipping prices and longer delivery times, was one of the significant themes for 2021.

Industry experts claim the current issues (ocean freight, container availability, low inventories) will continue throughout the first half of 2022, with little relief expected until late in the year. Newly added woes include the effect of the Russia-Ukraine conflict, with sanctions causing delays and putting a pressure on global supply systems, according to Maersk. The current environment is expected to limit major amounts of commodities entering North America from Asia, suppliers/traders will be unable to take advantage of the large regional arbitrage, and the U.S. market will remain more "local" for longer.

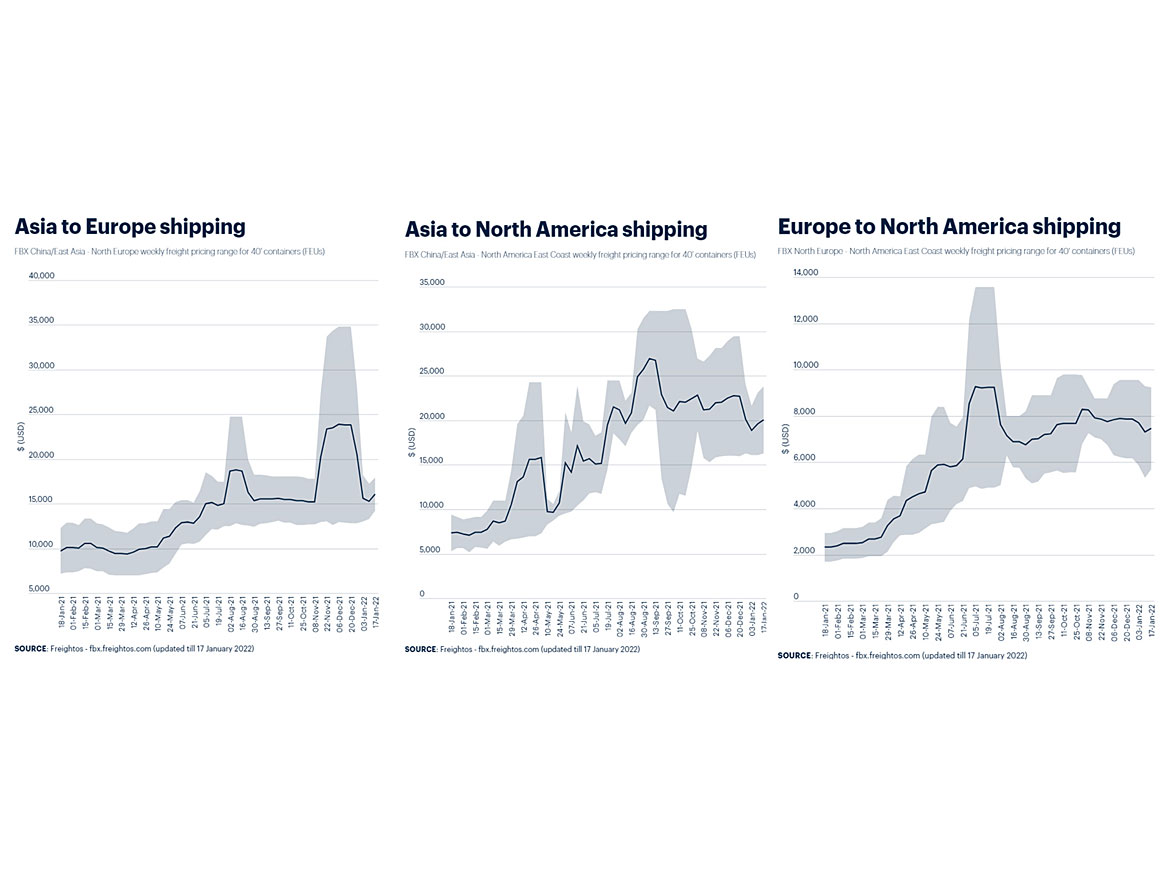

The global container crisis has also disrupted chemicals supply — “the public and media can’t grasp the complexity of the logistics situation, especially as it relates to politics, personnel and internal logistics,” according to a former high ranking public Ports official. Normal flows of products have been delayed or cancelled due to a lack of available capacity, and prices have spiked to unsustainable levels (Figure 6).

Conflict in Ukraine

Following Russia's recent invasion of Ukraine, governments quickly imposed economic sanctions on Russia. Moreover, a rising number of chemical companies are vehemently denouncing the country's conduct and thus breaking connections with it.

As of this writing, this conflict’s impact on chemical markets includes, but is not limited to:

- LyondellBasell to suspend, exit all business with Russian state-owned companies;

- Dow halts Russia investments, limits supplies to essential goods;

- Novozymes to stop shipment of products to Ukraine, Russia, Belarus;

- Clariant has halted all operations in Russia;

- The Russian invasion of Ukraine has shut down an ammonia pipeline and halted Black Sea exports, causing ammonia prices to rise.

As a result of the conflict, Russia's oil and gas supplies are in jeopardy: escalation might limit or halt supply to Europe as a result of retaliatory measures.

Overall, we can expect the invasion of Ukraine by Russia to raise the cost of producing petrochemicals, especially if Russian oil and gas exports are curtailed as part of international sanctions.

Nord Stream 2: How Does the Pipeline Fit into Ukraine-Russia Crisis?

Europe's most divisive energy project, Nord Stream 2 (worth $11 billion) was finished in September of 2021 but has stood idle pending certification by Germany and the European Union. Energy is a major political issue in central and eastern Europe, where gas supplies from Russia play an essential role in power generation and home heating. Natural gas prices have set new records this winter in Europe, and the conflict in Ukraine is bringing more pain to consumers.

The pipeline was designed to relieve pressure on those consumers who are suffering record energy prices as part of a wider post-pandemic cost-of-living crisis, as well as to governments that have already spent billions to attempt to mitigate the impact on consumers.

The Russian state-owned gas giant Gazprom owns the entire pipeline but paid half the costs, with the rest shared by Shell, Austria’s OMV, France’s Engie and Germany’s Uniper and Wintershall DEA (BASF owns roughly 67% of that company).

Critics however say Nord Stream 2 pipeline is more of a tool of Russian foreign policy — and there has been strong opposition from the U.S., Ukraine and Poland. The U.S. is concerned that the pipeline will make Europe far more reliant on Russian energy, giving Russian President Vladimir Putin tremendous clout over Berlin and the EU. UK Defense Secretary Ben Wallace has called the pipeline a "piece of leverage" the West can use against Moscow.

Based on the threat of Russia’s invasion, the Federal Network Agency — which regulates Germany's electricity, gas, telecommunications, post and railway sectors — had suspended the certification process in November, saying Nord Stream 2 must register as a legal entity in Germany. Germany imports half of its gas from Russia and has stated that Nord Stream 2 is essentially a commercial project aimed at diversifying Europe’s energy supply (Figure 7).

Following the invasion, “I think Nord Stream 2 is now dead,” Undersecretary of State for Political Affairs Victoria Nuland told U.S. lawmakers about the Kremlin's prize geopolitical energy project that became a victim of Western sanctions.

Conclusion

While there will obviously be more bumps in the road (rising rates, currency headwinds, freight issues and continued inflationary concerns), the environment for both coatings and adhesives producers, whether raw material suppliers, manufacturers, distributors or other members of the value chain, should be somewhat more "stable" than in 2021, with solid demand expected from the major end markets.

However, as we have said during many industry events this past year, including in Dan Murad’s Keynote address at Coatings Trends and Technologies in September 2021, do not expect a return to the old normal.

Companies need to aggressively pursue new ways of doing business, specifically e-commerce for sales, including being less reliant on single sources of supply in procuring goods, more invested in innovation pipelines to introduce new products especially those that address labor pool shortages, deeper paths of vertical integration to maintain self-sufficiency, and stronger consideration and definition of sustainable practices to address consumer demands and climate considerations.

We anticipate 2025 to look quite different from the start of the decade.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!