Chloride-Grade TiO2 Performs Well in 2015

Despite Depression of China’s TiO2 Industry

Figure 1

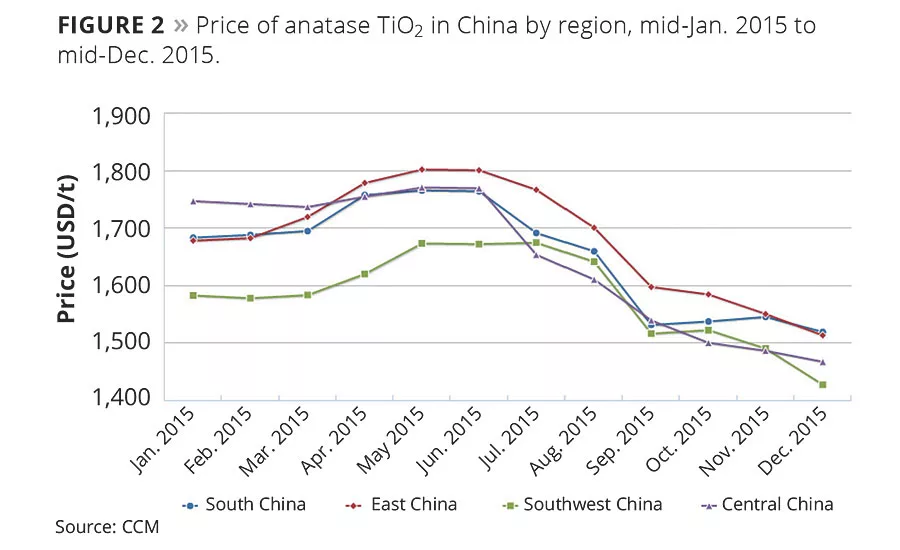

Figure 2

After 2011, the explosive growth of China’s real estate industry halted and the golden development period for TiO2 ended. In spite of this, TiO2 capacity still expanded uncontrollably. The consequences of severe low-end product overcapacity were exposed in the second half of 2015 (H2 2015). A major imbalance between supply and demand caused a collapse of TiO2 prices in China’s market. This article will summarize TiO2 market conditions in China in 2015 as well as some of the results of those conditions.

2015 Market Price Fluctuations

H1 2015

After market adjustments during the Chinese Lunar New Year, the declining trend that was initiated at the end of 2014 finally abated and the market price remained stable before increasing during March and May. This activity was stimulated by Shandong Doguide Group Co., Ltd. and Shandong Dawn Group Co., Ltd. Prices rose from USD 1,830.97/t (RMB12,000/t) to USD 1,907.26/t (RMB 12,500/t).

H2 2015

As a consequence of the long-term imbalance between supply and demand, the market price collapsed entering the second half of the year, and even the traditional peak sales season (September and October) could not save the market, with the price continuing to fall. In December, the transaction price of major sulfate-grade rutile TiO2 product dropped to below USD 1,449.52/t (RMB9, 500/t), almost equal to mainstream producers’ production costs. The rate of decrease reached 24% compared to that in H1 and plummeted by over 50% compared to the peak of USD 3,051.62/t (RMB 20,000/t) in 2011 (Figures 1 and 2).

The collapse in price has directly led to the successive suspension of production by many small- and medium-sized enterprises, such as Jiangxi Tikou Titanium Co., Ltd. and Luohe Xingmao Titanium Industry Co., Ltd. Even large-scale enterprises like Henan Billions Chemicals Co., Ltd. and Shandong Doguide Group Co., Ltd. reduced their operating rates slightly at the end of the year.

As a result, China’s total TiO2 output in 2015 (2.32 million tonnes) fell for the first time in 17 years, the last time being 1998, with a year-on-year decrease of 4.6% compared to some 2.44 million tonnes in 2014, according to the TiO2 Sub-Center of the Chemical Industry Productivity Promotion Center of China.

Of the total output of TiO2, 1.72 million tonnes was rutile TiO2, decreasing by 2.4% year on year and accounting for 73.8% of the total; 417,000 tonnes was anatase TiO2, accounting for 18% of the total; 128,000 tonnes was nonpigment-grade TiO2, accounting for 5.5% of the total, and 629,000 tonnes was denitrating TiO2 or nano TiO2, accounting for 2.7% of the total.

From the perspective of market price and output, China’s TiO2 industry bottomed out in 2015. Despite this, CCM believes that this was just a period of industry structure adjustment that had to be faced after going through a period of high overcapacity.

Catalyst for Reform

From another point of view, compared to the deathly stillness and lack of movement and innovation in the past two years, the hopeless market conditions of 2015 have, in fact, become a great catalyst for reform in the industry. A market price that was almost equal to production cost was just like a sudden clap of thunder, waking up speculators who were expanding capacity regardless of what it took during the peak period.

With obsolete capacity being forced out of the market, CCM believes that a highly dispersed industry will enter a period of consolidation, and the structure of capacity will tend to balance out, which will help China’s TiO2 industry to return to the right track within three to five years.

Achievements During Industry Restructuring

Good performance was still achieved during a period of industry restructuring and under depressed conditions. On May 5, 2015, Henan Billions announced that it was acquiring Chinese leading TiO2 company, Sichuan Lomon Titanium Co., Ltd., and with that, the first international-level Chinese TiO2 giant was born. Currently, the TiO2 capacity of Sichuan Lomon reaches 300,000 t/a and that of Henan Billions stands at 220,000 t/a, ranking No.1 and No.2 respectively in China. After the marriage between the two, a total capacity as high as 520,000 t/a will make it the fourth largest TiO2 company in the world. At that time, the international competitiveness and global market share of China’s TiO2 industry will be improved significantly.

A second achievement was that domestically produced chloride-grade TiO2 began to gain international recognition. In Nov.-Dec. 2015, Henan Billions vigorously marketed its chloride-grade TiO2 at the ChinaCoat exhibition. Its long-term partner, international coating magnate PPG Industries, Inc., announced on its official website that they had begun to use chloride-grade TiO2 produced by Henan Billions to produce coatings and thought highly of the product quality.

On Nov. 12-14, 2015, at the annual meeting of TiO2 producers, CCM learned from Li Mao’en, the President of Luohe Xingmao, which is the only privately operated chloride-grade TiO2 company in China, that their chloride-grade TiO2 products had been selling abroad widely and even their TiO2 exclusively for use on plastics had gained a good reputation.

On Dec. 30, 2015, Pangang Group Vanadium Titanium & Resources Co., Ltd. released an announcement revealing that they planned to invest USD 16.78 million (RMB 110 million) to build a chloride TiO2 project and to become the fifth Chinese company to enter the field.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!