Conflicting Views of the Near-Term Market Explained

Xiaoxing Zhao / Creatas Video, via Getty Images

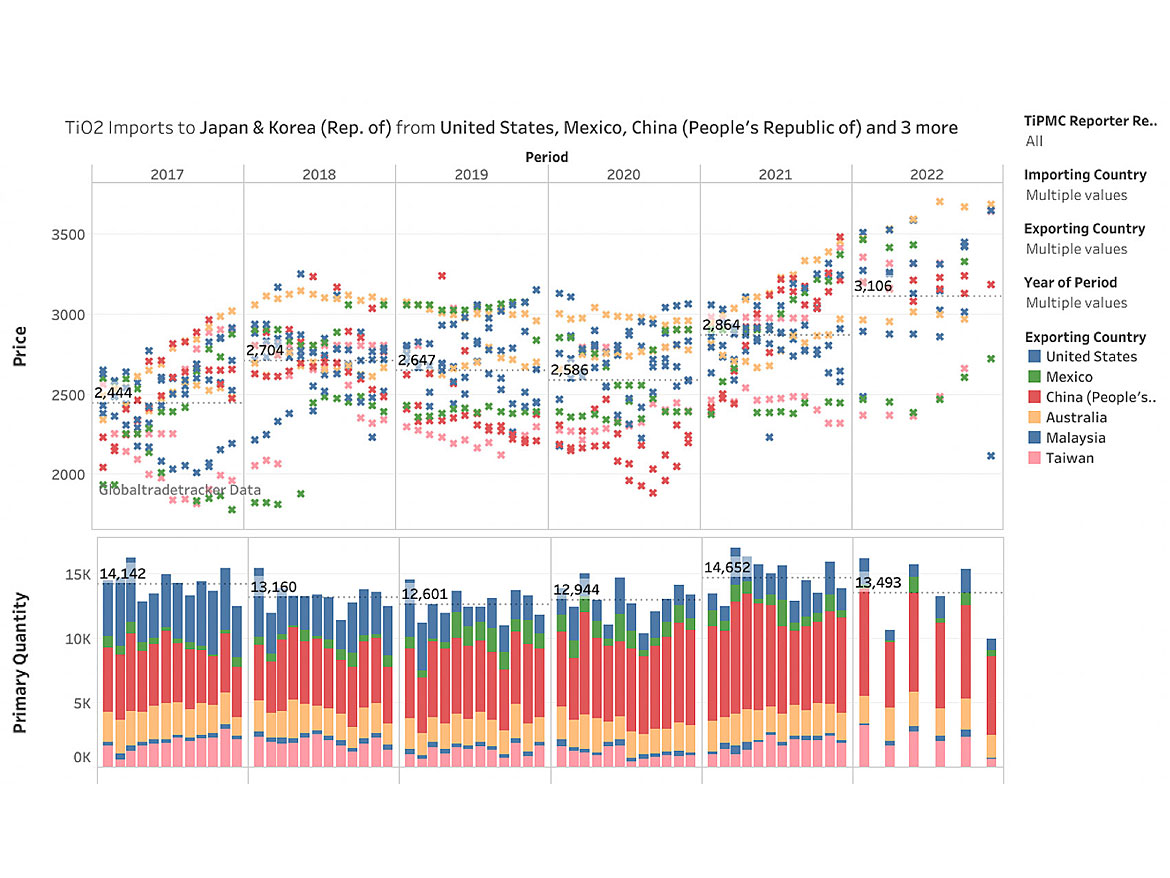

Results from major coatings and TiO2 manufacturers created a complex picture of the near-term future for the TiO2 industry. The consensus opinion of leading executives was there are many signs of slowing markets in Europe and parts of Asia, particularly China. Energy inflation throughout Europe, particularly Germany, and COVID-19-related lockdowns took their toll on TiO2 demand. Import statistics to Japan, Korea, and Germany support these claims.

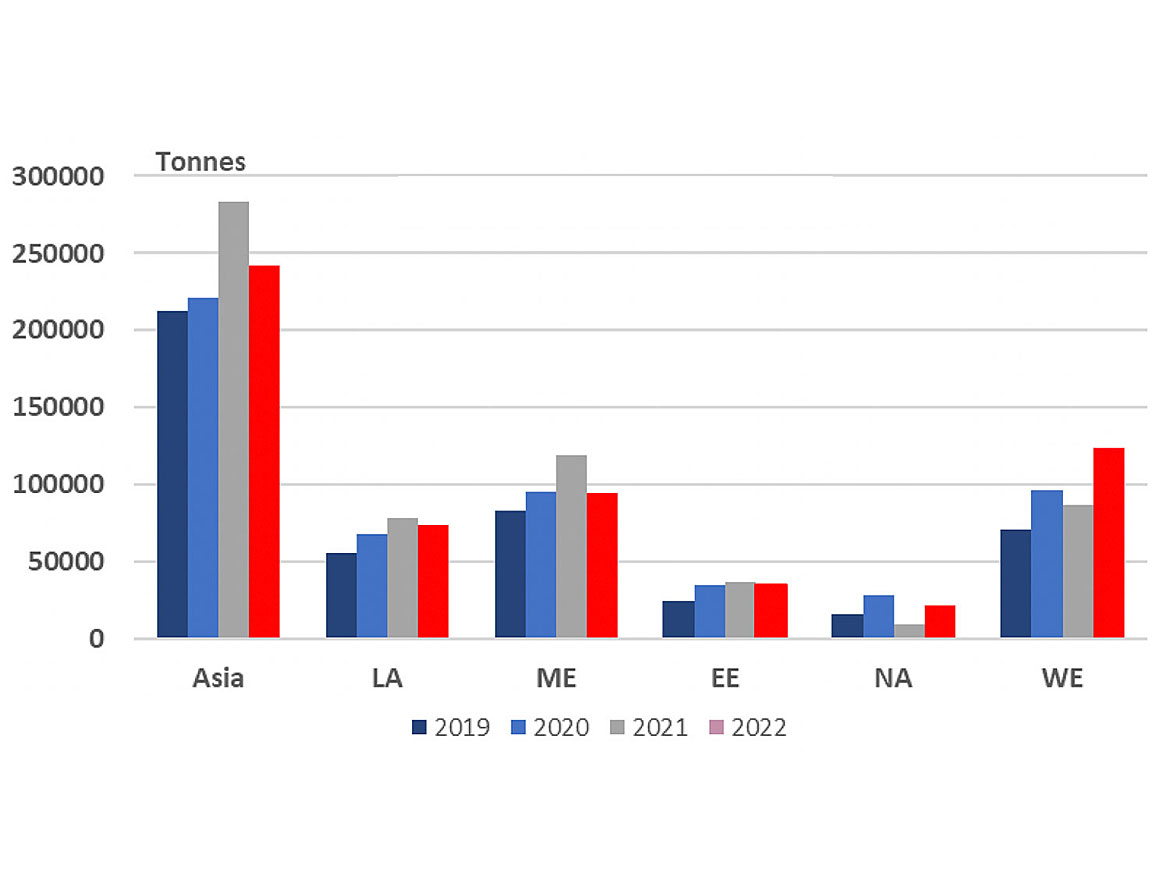

FIGURE 1 ǀ 2018-2022: TiO2 import volumes into Germany.1

TiO2 exports from China increased beyond normal levels, indicating domestic demand for TiO2 is suffering, as the pandemic and a slow real estate market weigh on coatings and other key materials, impacting TiO2 demand. As TiO2 prices in Europe increase monthly and energy surcharges are applied, Chinese exports to Europe have risen substantially. DIY is slowing in Europe and the United States. The major bright spots are professional paint markets in North America and southern Asia. How are TiO2 producers still seeing low stocks throughout the chain and forecasting higher prices in quarter three this year?

TiPMC believes a key element overlooked centers around the lack of investment by global TiO2 players. Despite global demand increasing by 1.5 M since 2016, net capacity expansion outside China has been negligible. Although China has increased capacity, Chinese capacity utilization during the period has risen dramatically, stressing their ability to fill the void. Overall industry utilization rates remain high.

Adding to the issue, TiPMC estimates the four large multi-national producers to have seen sales drop by nearly 70 kt (4%) vs. 2021, despite sold out markets. Lack of available titanium feedstock, plant maintenance issues, and environmental restrictions on waste processing were major causes of production disruption during the first half of 2022.

What Does it Mean for TiO2 Consumers and What Can be Expected in The Future?

TiPMC believes multi-national TiO2 producers (MNPs) are extremely conscious of generating cash through disciplined capital spending. Following a decade of steadily increasing Chinese exports eroding their market share, MNPs are focusing their efforts on stable pricing, cost reduction, and maintaining the advantages of back-integration into feedstock, including benefitting from the zircon market, remaining tight for the foreseeable future.

TiPMC believes the current trends are further evidence of an increasingly differentiated market for TiO2. MNPs are willing to forego lower-value business versus expanding facilities to meet the needs of the full market. Not only will expansion outside of China be very limited, but further plant closures are expected.

The result is an industry tighter in supply, with more stable, but higher prices for higher-end consumers. Chinese-supplied consumers will see higher fluctuations in price and supplier reliability.

For more insights into the TiO2 and Mineral Sands markets, visit TiPMCconsulting.com, or see our ad in this issue for more details. For more information about the impact price stabilization on the TiO2 industry, ask to see our latest issues.

1 Global Trade Tracker / Tableau® for TiO2.

2 Global Trade Tracker.

3 Global Trade Tracker / Tableau® for TiO2.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!