Why Life Cycle Assessments Are Becoming the Financial Framework for Paint and Coatings Sustainability

Need to Know

- Life cycle assessments quantify environmental impacts at the product level, enabling coatings formulators to compare materials, processes and performance tradeoffs.

- Product carbon footprints provide a simplified climate metric, but multi-attribute LCA results are required to avoid burden shifting across impact categories.

- Durability, service life and repaint frequency often dominate cradle-to-grave impacts, making performance a key sustainability driver in coatings.

- Product Category Rules and Environmental Product Declarations standardize LCA methodology and reporting, improving comparability and credibility across suppliers.

- Organizations that integrate LCA into R&D, procurement and operations can align product design with corporate sustainability targets and customer requirements.

Sustainability in paint and coatings is transitioning from voluntary messaging to performance that must be measured, governed and verified. Across architectural, industrial, protective and OEM coatings, customers are seeking coatings that a) have lower carbon emissions, b) contain renewable or recycled content and c) are safer for manufacturers and for their intended downstream users. In addition to product-related targets, most coatings companies have near-term 2030 commitments that require measurable progress.

A practical way to understand this shift is to treat product sustainability information as an accounting system. Corporate sustainability reporting provides a consolidated view analogous to corporate financial statements, while product Life Cycle Assessments (LCAs) can provide unit-level environmental “cost” accounting. Product Category Rules (PCRs) and Environmental Product Declarations (EPDs) play a role like accounting standards and audited disclosures, enabling comparability and customer trust.

Market Context: Why Coatings Sustainability Is Now Business-Critical

Paint and coatings’ sustainability profiles influence both consumer choice and industrial outcomes. In architectural coatings, low odor, low VOC and safer-chemistry expectations shape retail demand. In construction, owners, architects and specifiers increasingly request product transparency to support embodied carbon targets and material disclosure compliance. In industrial and protective coatings, durability and corrosion protection drive maintenance cycles, downtime and total cost of ownership, making sustainability inseparable from performance. Extended Producer Responsibility (EPR) regulations will impact these markets to varying degrees by end-product categories as they are rolled out in the EU and state by state across the United States.1

The typical sustainability levers that address the above dynamics include:

- transitioning manufacturing plants to use renewable electricity,

- increasing renewable content in input raw materials and products,

- shifting to lower carbon feedstocks in binder and pigment supply chains,

- raising solids levels and optimizing application efficiency,

- reducing transport and packaging burden,

- minimizing waste and supporting programs that responsibly collect it,

- choosing recycled content in packaging and

- eliminating substances of concern all the while preserving paint performance.

The differentiator is the ability to quantify outcomes consistently and credibly.

Corporate Sustainability vs Product Sustainability: Two Ledgers, Two Decisions

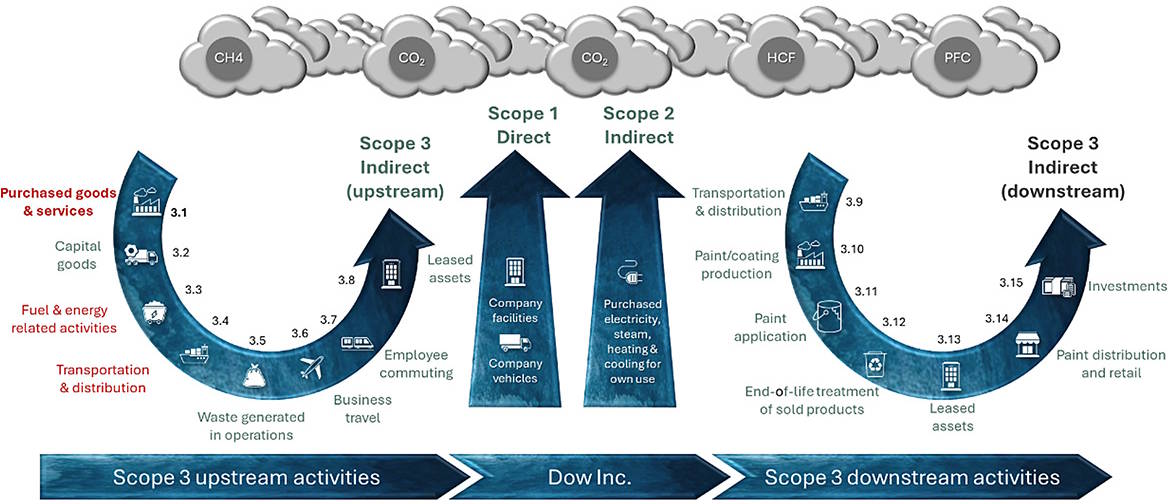

Corporate sustainability tracking aggregates enterprise performance, Scope 1 and 2 emissions from sites and Scope 3 estimates across upstream purchased goods, logistics and downstream stages (Figure 1). While difficulties have emerged in collecting Scope 3 emission data across all categories, this entirety of Scope 1–3 data supports governance, supplier engagement and public commitments.

Click to enlarge

GHGs: CO₂ (carbon dioxide); CH4 (methane); N₂O (nitrous oxide); HCFs (hydrofluorocarbons); PFCs (perfluorocarbons); SF6 (sulfur hexafluoride)

Source: GHG protocol, Dow modified for paints and coatings.

Product sustainability asks: What is the impact per unit of function delivered by a coating system? In coatings, “per kilogram” can be less meaningful because value is delivered through beauty, color, coverage, dry film thickness, durability and time between repaints. A premium architectural paint that lasts longer can reduce lifetime material use, contractor travel and repainting labor costs, as would a high-performance anticorrosive system that may have higher environmental impact per kg of paint produced but lower impact per year of protection if it extends recoat cycles.

Finance provides an analogy: Corporate financial reports are consolidated statements as are sustainability reports that aggregate companywide impacts. In contrast, product LCAs are akin to unit economics where cost per produced unit ($/kg) is replaced by environmental impact characterization factors that are applied to impact contributors and these are then rolled up for a binder or a paint. Organizations that connect both can prioritize R&D and capital expenditure where they improve both corporate targets and allow for product differentiation.

Product Category Rules (PCR) and Environmental Product Declarations (EPD): Sustainability Standards and Disclosures

Customers want comparability across suppliers and this is difficult without shared rules. PCRs define the framework for how an LCA must be conducted. This is a critical step for enabling comparability across studies and suppliers. Also important are functional units tied to area applied, film thickness and service life (market and/or design life with performance properties impacting the latter); system boundaries; allocation rules; treatment of packaging and transport; and the required impact categories along with their methodologies.

EPDs present the LCA results in a standardized summary disclosure format and verification is required to achieve credits in most green building certifications. In building and construction ecosystems, EPDs support material selection and embodied carbon calculations. For manufacturers, they impose helpful discipline via transparent documentation, repeatable modeling and results that can withstand external scrutiny.

Conceptually, Product Category Rules (PCRs) are like accounting standards such as GAAP or IFRS by defining consistent calculation and reporting rules, while Environmental Product Declarations (EPDs) function like standardized, verified disclosure statements except being focused on product-level environmental impacts rather than financial performance. The current standard for PCRs and EPD is ISO 21930 and 14025.2,3 These are living standards continually being refined and improved like all good quality systems.

What Is a Life Cycle Assessment (LCA) and What Is Its Output?

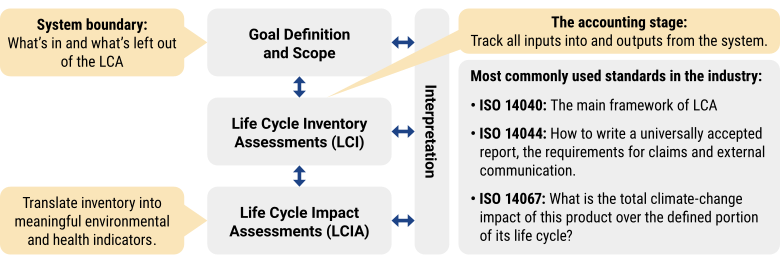

LCA quantifies environmental impacts across a product’s life cycle and is usually conducted according to prescribed and accepted international standards. ISO 14040/14044 are the overarching standards for LCA studies and describe the requirements that include four phases: goal and scope, inventory (LCI), impact assessment (LCIA) and interpretation. Full LCAs conducted under ISO 14040/44 quantify many impact categories such as climate change, acidification, eutrophication and smog formation to name a few. ISO 14067 addresses only climate change impacts and may be applied to either the full life cycle or a defined subset of life cycle stages, depending on study scope (Figure 2).

In coatings, the lifecycle inventory (LCI) includes masses of binders, pigments, fillers, solvents and additives; energy used in manufacturing; yields and losses; packaging weight; and transport distances. Lifecycle Impact Assessment (LCIA) converts inventory into impact categories such as global warming potential (GWP), acidification, eutrophication, photochemical ozone formation (smog), resource depletion and water use. Some methods also include toxicity-related indicators. As with financial statements, the credibility of the output depends on documented assumptions, data quality and appropriate independent review when used externally.

Figure based on ISO 14040 standard protocol.

Credit: Dow

LCA Types That Matter Most in Coatings

Baseline LCAs establish an impact footprint and identify hotspots, often the foundation for an EPD. Comparative LCAs evaluate alternatives under a consistent functional unit and consistent assumptions, supporting decisions like binder technology substitution, pigment package optimization or packaging redesign.

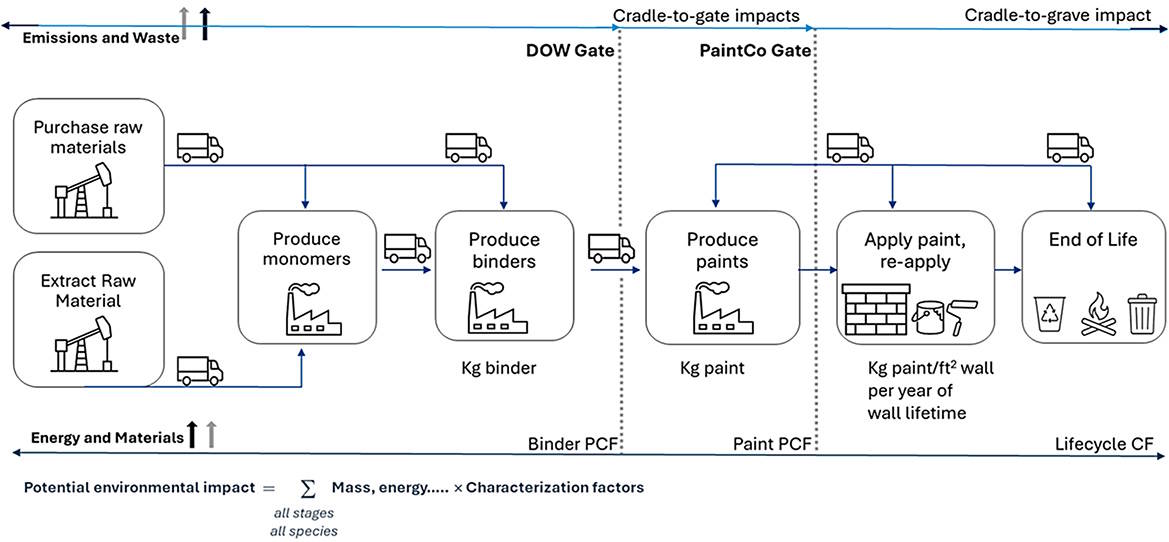

Boundary choice is equally important. Cradle-to-gate includes upstream materials and manufacturing through the factory gate and is common for supplier comparisons. Cradle-to-grave adds distribution, application, repainting cycles and end-of-life (Figure 3). This type of LCA is essential for architectural paints and protective and maintenance coatings because service life and repaint frequency can dominate total impacts and this is specified for EPDs.

Click to enlarge

Coating-Specific Hotspot Patterns

While every formulation is distinct, paint LCAs often reveal consistent patterns that help organizations focus improvement efforts. In cradle-to-gate studies, upstream raw materials such as TiO₂ and binders contribute disproportionately to the environmental impacts with lesser impacts from paint production, packaging and transportation.4,5 For paint production, emissions from plant energy use is a small portion of the paint’s overall carbon footprint but is a lever within a company’s control because site electrification with renewable power can reduce Scope 2 carbon emission impacts across many paint SKUs simultaneously.

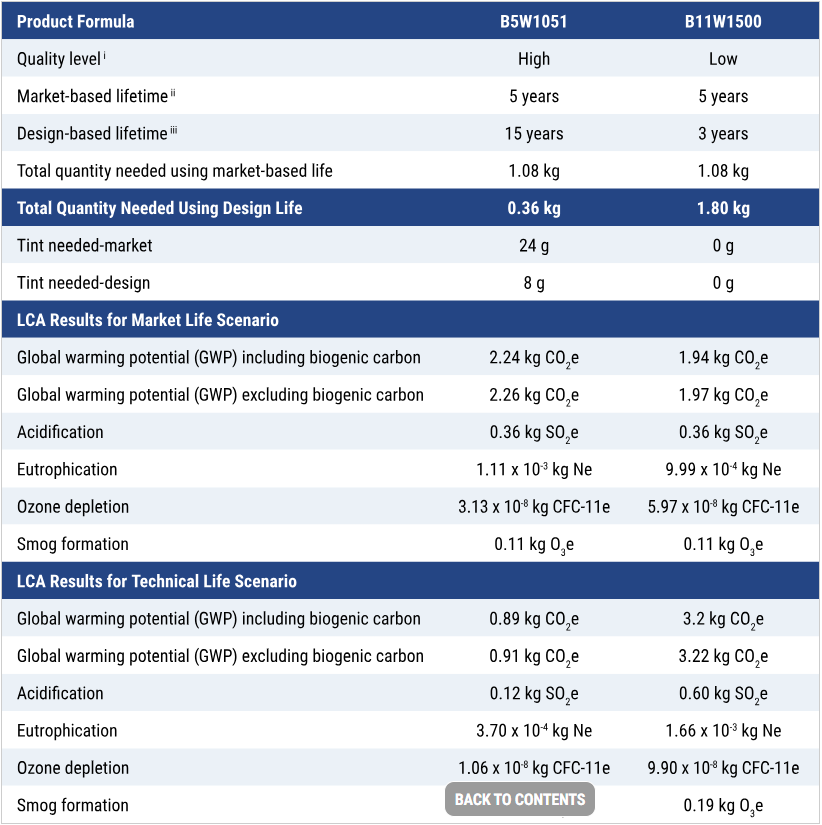

In cradle-to-grave studies, durability and repaint frequency can become the dominant drivers. A coating system that extends maintenance intervals can reduce lifetime material consumption, application energy and waste even when its cradle-to-gate footprint is slightly higher. This is why functional unit selection and performance equivalence are strategic issues, not just technical footnotes. Most environmental impacts from high quality paints are lower when paints remain on the wall for their intended technical lifetime. Customer choice to repaint does of course play a role in this decision (Table 1).6

Table 1. Comparison of LCA impacts for a high- and low-quality paint reported in a published EPD.

Click to enlarge

Functional unit for the study was the paint (kg) needed to cover and protect 1m2 of substrate for a period of 60 years (the assumed lifetime of a building).

Notes:

- Quality level is defined in the Product Category Rule for interior paints.

- The estimated lifetime of a coating based on the actual use pattern of the product type by the end consumer. In this instance, a repaint may occur before the coating fails.

- The estimated lifetime of a coating, based solely on its hiding and performance characteristics determined by results in certain ASTM durability tests.

PCF and Multi-Attribute Thinking: Avoiding Single-Metric Optimization

Product Carbon Footprints (PCFs) report greenhouse gas emissions as kg CO₂e per functional unit or a declared unit under a defined system boundary and are widely requested because they easily integrate into customer decarbonization programs. But coatings are chemically complex systems and PCF is not a simplified LCA. A change that reduces GWP can shift burdens to smog formation (e.g., VOC levels and solvent changes), eutrophication or acidification upstream (e.g., agricultural inputs for some bio-based feedstocks), or toxicity-related indicators depending on substitutions. Multi-attribute LCA results help teams avoid the “carbon-only” emphasis that creates other risks such as selective benefit promotion. Regardless of just PCFs or other impacts, great rigor as described in Annex B of ISO 14067 must be applied when comparing impacts.7

PCF comparisons for fossil versus bio-based or mass-balance binders require clarity on biogenic carbon treatment, co-product allocation and end-of-life assumptions. The best practice is to treat these like financial estimates: disclose methods, run sensitivities, seek external review and validation when used for external claims and report with the transparency prescribed in guidelines such as Together for Sustainability (TfS).8 An illustrative example for a PCF report is presented below (Table 2).

Table 2. Pro forma PCF report for a biomass-balanced paint binder.

Paint Binder A (Biomass Balanced)

Product Carbon Footprint Report

Methodology:

- ISCC+ mass balance for plant-based feedstocks

- Standards: ISO 14040 / 44 (2006)

- Together for the Sustainability (TfS): “Product Carbon Footprint Guideline for the Chemical Industry, Version 3.0, December 2024.”

- Primary data: 2024 production year — 12-month continuous production

- Secondary data: Ecoinvent 3.xx database

- Software: SimaPro ver. xx.yy

- Carbon content:

- Biogenic carbon = xx kg carbon / kg binder

- Total carbon content = yy kg carbon / kg binder

Reporting:

- Boundary: Cradle to binder factory gate

- Value: kg CO2e per kg of product.

Exclusions:

- All lifecycle stages beyond cradle to gate — such as paint production with the binder, paint use on wall, and end-of-life assessments — are excluded.

| Impact Category (GWP) | Paint binder A* (Petrochemical based) |

Paint Binder A* (Biomass Balanced) |

|---|---|---|

| Total global warming potential (GWP) | 2.20 kg CO2e/kg | -0.39 kg CO2e/kg |

| GWP-fossil | 2.20 kg CO2e | 1.80 kg CO2e |

| GWP-biogenic CO2 removals | 5.10 x 10-4 kg CO2e | -2.20 kg CO2E |

| GWP-biogenic CO2 emissions | 2.90 x 10-3 kg CO2e | 5.80 x 10-3 kg CO2e |

| GWP-direct land use change (dLUC) | 2.70 x 10-4 kg CO2e | 2.68 x 10-4 kg CO2e |

| GWP-aviation emissions | 1.20 x 10-7 kg CO2e | 1.18 x 10-7 kg CO2e |

* Numbers are for illustrative purposes only to show the scales.

Data Variability and Governance: Making Sustainability Accounting Audit-Ready

LCA methodology is standardized but much younger than financial reporting and results can vary with choices and datasets. In coatings, major sources of variability include functional unit and durability assumptions; allocation methods (co-products and recycling); data quality of background datasets (geography, age, technology); impact method; the LCA software type and the primary databases from which data is pulled for analysis.

Governance reduces variability over time. Leading organizations define modeling rules aligned to relevant PCRs, maintain an approved dataset library, prioritize primary supplier data for hotspot inputs (binders and pigments) and implement version control with change logs. External critical review, especially for comparative LCAs and EPDs, functions like an audit by checking conformance, transparency and internal consistency. They also act as a bulwark against claims of “greenwashing,” by separating the slapdash versus the scrupulous.

Implementation Roadmap: Building an LCA Capability Like a Finance Process

Organizations that succeed treat LCAs as a repeatable business process rather than a one-off technical study.

A practical process often includes:

- agreeing on decision use cases (full LCAs, customer PCF requests, R&D screening, portfolio optimization),

- standardizing functional units for key segments (architectural interior, architectural exterior, industrial OEM, protective) and deciding on the methodological frameworks for the LCA,

- defining a data model linking formulations, packaging and site energy,

- establishing a data hierarchy for hotspot inputs and

- implementing review gates and documentation templates.

Many functions and roles contribute to inputs when conducting an LCA. R&D and technical service own formulation and performance equivalence assumptions; procurement supports supplier data collection; operations provides site energy and yield data; and sustainability provides standards alignment and disclosure governance. When these roles and contributions are defined, LCAs can be updated on a cadence, like closing the accounting books, supporting faster customer responses and more confident product strategy.

Conclusion: LCAs as the Backbone of Coatings Transparency

In paint and coatings, credibility for sustainability claims is increasingly earned at the product level. LCAs connect formulation and manufacturing decisions to measurable outcomes, PCRs provide comparability rules and EPDs provide trusted disclosure. PCFs enable rapid climate-focused engagement, while full LCAs protect against unintended tradeoffs.

As transparency expectations expand, especially in markets influenced by EU policy, LCA-based reporting will grow beyond climate change impacts to broader impact categories. PCF reporting platforms such as SiGreen are a good step in this direction. Companies that manage LCAs like financial statements, standardized, documented and reviewable will be the best positioned to win customer trust and to compete for success.

References

¹ Cassel, S.; Aldred Cheek, K. EPR achievements: The case of paint in the United States. Coatings World 2019, 40–43. https://productstewardship.us/wp-content/uploads/2023/05/EPR-Achievements-The-Case-of-Paint-in-the-U.S.-Published.pdf

² International Organization for Standardization. Sustainability in Buildings and Civil Engineering Works—Core Rules for Environmental Product Declarations of Construction Products and Services (ISO 21930:2017); 2017. https://www.iso.org/standard/61694.html

³ International Organization for Standardization. Environmental Labels and Declarations—Type III Environmental Declarations—Principles and Procedures (ISO 14025:2006); 2006. https://www.iso.org/standard/38131.html

⁴ Middlemas, S.; Fang, Z. Z.; Fan, P. Life cycle assessment comparison of emerging and traditional titanium dioxide manufacturing processes. Journal of Cleaner Production 2014, 89, 137–147. https://doi.org/10.1016/j.jclepro.2014.11.010

⁵ PPG Architectural Finishes, Inc. Environmental Product Declaration (EPD): SPEEDHIDE® Zero Interior Architectural Coatings, Declaration No. EPD10074; NSF International, 2016. https://info.nsf.org/Certified/Sustain/ProdCert/EPD10074.pdf

⁶ The Sherwin-Williams Company. Harmony® Product Line Environmental Product Declaration (EPD) Action Plan (EPDAP 106); NSF International, 2021. https://info.nsf.org/Certified/Sustain/ProdCert/EPDAP-106.pdf

⁷ International Organization for Standardization. Greenhouse Gases—Carbon Footprint of Products—Requirements and Guidelines for Quantification (ISO 14067:2018, Annex B); 2018. https://www.iso.org/standard/71206.html

⁸ Together for Sustainability (TfS). The Product Carbon Footprint Guideline for the Chemical Industry: Specification for Product Carbon Footprint and Corporate Scope 3.1 Emission Accounting and Reporting (Version 3.0, Sec. 3.3.2.4, “Biogenic Emissions and Removals”); 2024. https://www.tfs-initiative.com/app/uploads/2024/12/TfS-PCF-Guidelines-2024.pdf

Explore more developments in sustainable coatings and how lifecycle thinking is shaping formulation strategies across the industry.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!