TiO₂ Market Shows Early Signs of a Turn

Signs of Recovery and Market Consolidation on the Horizon

After a difficult year of slumping demand and squeezed margins, the global titanium dioxide (TiO₂) industry is cautiously optimistic that 2026 will mark the start of a recovery.

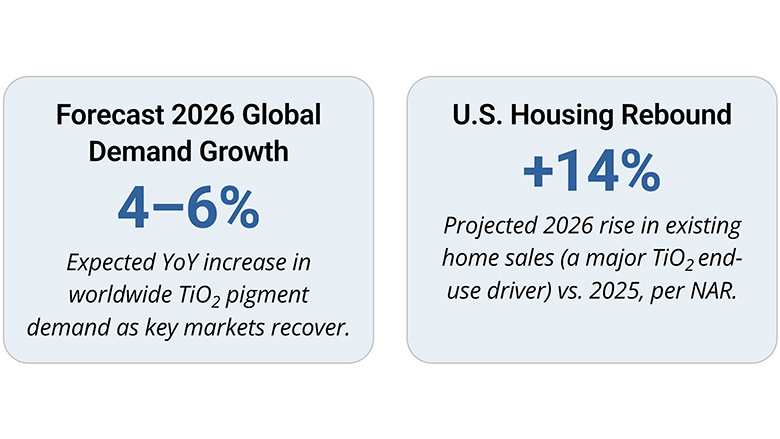

The past year (2025) saw steep declines in earnings and cash flow, leaving many producers with high financial leverage. However, multiple positive indicators are emerging. Global TiO₂ demand is currently well below its 50-year trend, suggesting room for above-GDP growth in the coming year. A key driver is the rebound in the U.S. housing market, where existing home sales are generally believed to be increasing as mortgage interest rates ease from last year’s peaks. Meanwhile, Asian markets are also showing renewed strength, with the IMF projecting Southeast Asia to be the fastest-growing region globally in 2026. High-growth countries such as India, which faced a weak second-half of 2025, are poised for a market rebound in the coming months.

Restocking dynamics are reinforcing these demand trends. TiPMC’s own index shows that customers ended 2025 with extremely lean TiO₂ inventories, especially in North America. This suggests that even a modest pickup in downstream demand will translate into substantial restocking orders for TiO₂ producers in early 2026 as paint, plastic, and paper manufacturers replenish their supplies.

Supply-side adjustments are also paving the way for a healthier market. Over the past 12 months, roughly 600,000 tonnes of TiO₂ capacity outside China – about 15% of non-Chinese global capacity – have been taken offline. This includes the insolvency of Venator Plc and the shutdown of its ~400,000 t pigment operations in Europe in September 2025, as well as Tronox’s closure of its 90,000 t Botlek (Netherlands) plant in late 2025. These drastic cuts, alongside earlier curtailments, have significantly reduced the Western TiO₂ supply overhang. By early 2026 the industry’s footprint is markedly leaner, and multinational producers are already reporting market share gains in regions formerly served by the now-idled capacity. Remaining TiO₂ suppliers are thus entering 2026 in a stronger position to raise operating rates and improve profitability.

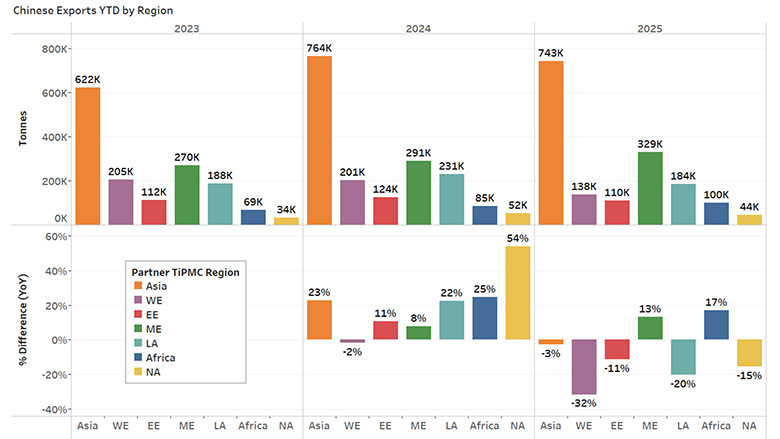

Global trade flows are also undergoing structural shifts. Chinese TiO₂ producers, now accounting for over half of world demand, have long relied on exports to balance their oversupply. But broad antidumping tariffs in regions like the European Union, Brazil, India, the UK, and Saudi Arabia are restricting nearly 40% of China’s export volume. These measures (with duties from ~16% up to 45%) have already driven Chinese TiO₂ exports down ~4.5% in 2025 compared to the prior year, with particularly sharp declines in shipments to Europe and Latin America. This trend is shifting more market share toward non-Chinese suppliers in those regions and forcing Chinese producers to focus on their domestic and other tariff-free markets. Notably, 2026 marks the first full year of these tariffs in the EU and Brazil – a development expected to further favor Western and regional Asian producers in those markets. In India, where official duties are still being finalized, Chinese TiO₂ prices have recently risen on higher costs, which should improve the competitiveness of global producers once import tariffs take hold.

On the pricing front, there are early signs that the price erosion of 2023–2025 may be bottoming out. With customer inventories now depleted and supply curtailed, TiO₂ suppliers have greater leverage to implement price increases – and many announced hikes in late 2025. Major Western producers signaled “value over volume” intentions by targeting price increments of $100–150 per tonne on various grades effective Q4 2025. While not all increases fully succeeded, declining stock levels and an uptick in orders appear to be supporting a firmer price environment. In China, leading pigment makers hiked domestic prices by over $200/ton in Q4 to offset surging sulfuric acid and energy costs. These moves, coupled with tariff shields in import markets, mean that Western producers are entering 2026 with some cautious pricing power for the first time in years. Indeed, TiPMC observes that global suppliers have largely returned to a disciplined stance, holding or raising prices rather than chasing volumes, especially for less strategic accounts. This pricing discipline – if maintained – should help margins recover as demand gradually improves.

Looking ahead, industry forecasters see 2026 as a pivotal transition year. TiPMC projects that world TiO₂ demand will rise on the order of 4–6% year-on-year in 2026, breaking the pattern of the past three years of stagnation and decline. Such growth, however modest, would outstrip overall economic expansion and reflect a return to more “normal” demand patterns as end-users move from destocking back to moderate restocking. Meanwhile, if producers continue to keep a rein on excess capacity, operating rates should climb, allowing for better cost absorption and potentially firmer pricing. Still, executives remain vigilant. Key risks include Europe’s sluggish recovery (dampened by the ongoing Ukraine conflict and high energy costs), as well as uncertainty in China’s property sector despite stimulus efforts. Nonetheless, the consensus among industry observers is that the worst of the downturn has passed.

Bottom Line: The TiO₂ sector enters 2026 on improved footing. Aggressive capacity cuts and a wave of consolidation have started to “right-size” the supply base, while global demand fundamentals are gradually turning upward. With lower inventories and favorable macro tailwinds – from Western housing to Asian growth – producers are poised to benefit from a long-awaited recovery. The next test will be whether they can capitalize on these conditions by maintaining pricing discipline and operational efficiencies in an evolving, more consolidated market. Only then will the TiO₂ industry’s nascent “recovery and reset” truly take hold.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!